The Strategic Window Is Open - For Now

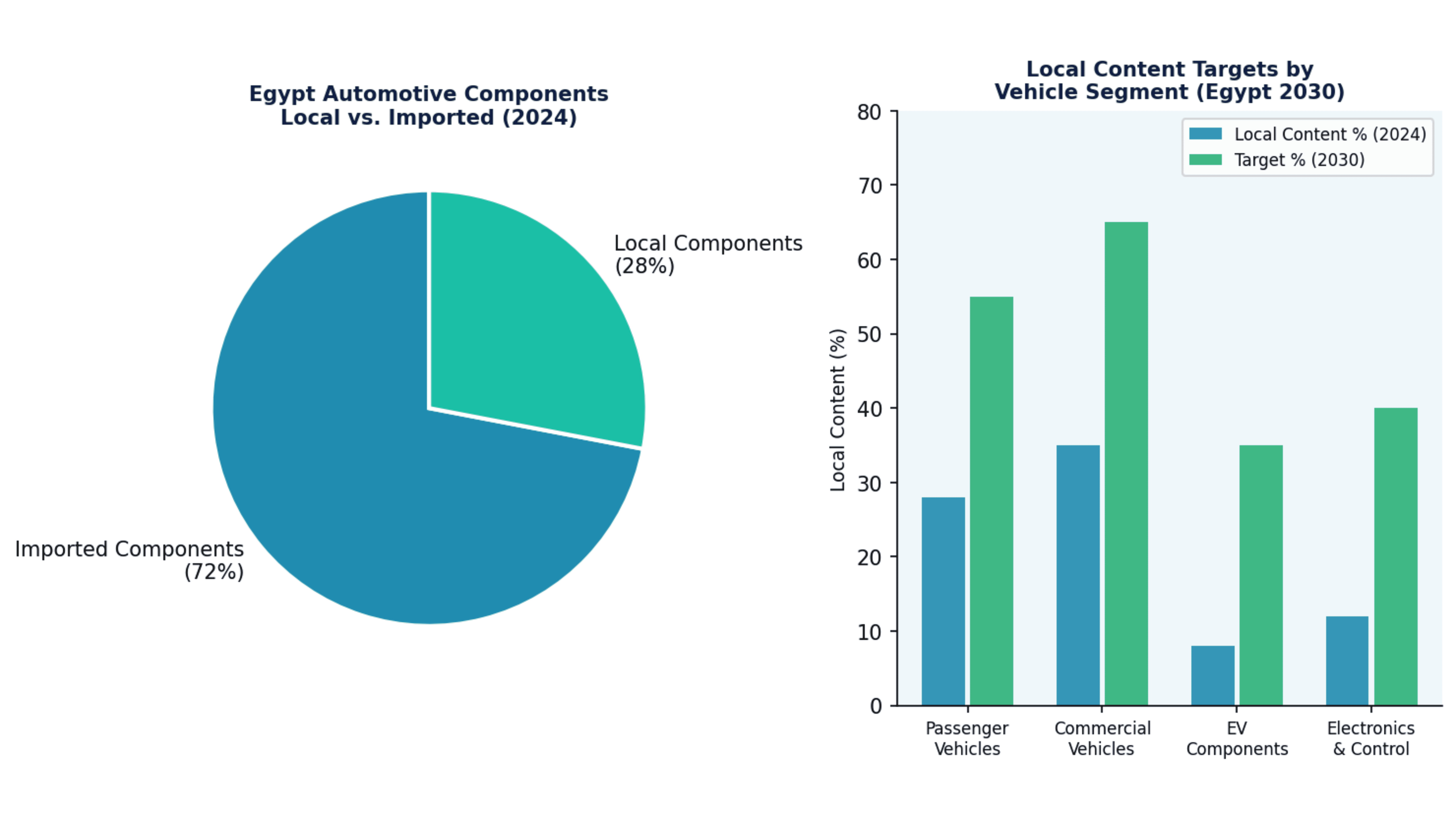

Egypt assembles vehicles. It does not yet manufacture them. That distinction carries a profound economic consequence: the assembly margin is thin, cyclical, and fully dependent on the decisions of foreign OEMs. The manufacturing margin, embedded in components, subsystems, and tier-1 supply, is where wealth accumulates, jobs multiply, and technological capability compounds. Egypt currently captures roughly 28% of its automotive value domestically. The remaining 72% is imported. Changing that ratio, even modestly, represents a multi-billion dollar industrial shift.

But the window for Egypt to build this capability is narrower than it appears. The global automotive sector is undergoing its most significant structural transition in a century, the shift from internal combustion engine (ICE) to electric vehicle (EV) platforms. The component sets are fundamentally different. ICE expertise is becoming obsolete. Egypt must decide whether to double down on traditional components while that market exists, pivot directly to EV-related manufacturing, or, the more defensible answer, build platform-agnostic manufacturing capabilities while selectively targeting high-value EV components.

Why Egypt's Current Supply Chain is Structurally Weak

Figure 1. Egypt Automotive Components: Local vs. Imported Share (2024) & Localization Targets by Segment (2030)

Egyptian automotive suppliers face four compounding disadvantages. First, scale: most Egyptian component manufacturers are SMEs operating at volumes incompatible with OEM quality systems. A Tier-1 automotive supplier must typically run Statistical Process Control (SPC), maintain PPAP documentation, and achieve Cpk values above 1.33, requirements that eliminate most Egyptian candidates at the first audit. Second, material science gap: precision metal components for automotive applications require controlled alloy compositions, heat treatment protocols, and surface treatment processes that are inconsistently available in Egyptian manufacturing infrastructure. Third, qualification time: earning supplier approval from a single global OEM takes 18–36 months under IATF 16949 and customer-specific requirements. This timeline alone prevents rapid supply chain development. Fourth, technical workforce: while Egypt produces strong mechanical engineers, the specialized disciplines of automotive NVH (noise, vibration, harshness), fatigue life testing, and functional safety (ISO 26262) are underrepresented in the technical labor market.

The Localization Opportunity: Where to Focus

Not all components are equal targets. A structured localization strategy should prioritize based on three criteria: local manufacturing feasibility (material and process requirements), value density (cost per kilogram and per unit), and OEM demand stability. Applying these filters identifies clear priority tiers for Egyptian supply chain development.

• Tier A - High feasibility, high priority: Seating and trim systems, wire harnesses, plastic interior components, rubber and NVH isolation components, battery enclosures and thermal management housing (for EV).

• Tier B - Medium feasibility, medium priority: Stamped structural components, aluminum castings for transmission and engine housings, brake system components.

• Tier C - Long-term/strategic: Electronic control units (ECUs), sensors, electric motors, battery management systems, require significant R&D investment and government partnership.

Building the R&D Infrastructure for Automotive Supply

The missing ingredient in Egypt's automotive supply chain is not factories, it is the validation infrastructure that proves Egyptian components can meet OEM specifications. This requires a dedicated automotive testing and qualification center with access to material characterization, fatigue and durability testing, EMC (electromagnetic compatibility) testing, and environmental simulation chambers. No single SME can finance this alone. The model that works in comparable markets, Morocco's automotive success story is instructive, is a consortium model: government anchor funding, OEM partnership, and R&D institution engagement to build shared qualification capacity.

Egypt has the academic talent at Cairo University, Ain Shams, and the Military Technical College to staff such a center. What is required is the orchestration architecture that connects this talent to commercial supply chain requirements.

The EV Transition: Risk and Opportunity Simultaneously

Egypt imports EVs from China in growing volumes, and the MENA region is forecast to see EV sales grow from 2,100 units in 2022 to over 42,000 by 2030. For Egyptian suppliers, this represents both a threat to existing ICE component investments and a unique opportunity: EV supply chains are newer, less consolidated, and more open to new entrants than ICE supply chains, which have been locked up by incumbent suppliers for decades. Egypt could realistically become a regional supplier of EV thermal management components, charging system hardware, and battery enclosures, all physically intensive, manufacturing-capable products that align with existing Egyptian industrial strengths.

Key Takeaways

• Egypt currently sources 72% of automotive component value from imports, changing this ratio by even 20 points represents a USD 3B+ annual industrial shift.

• The EV transition creates a window for new entrants: EV supply chains are less consolidated than ICE equivalents and more accessible to manufacturers who move early.

• Success requires shared qualification infrastructure, IATF 16949 alignment, and a government-OEM-R&D institution consortium model.

• Priority targets: seating/trim systems, wire harnesses, plastic interiors, and EV thermal management components.

References

[1] Moroccan Automotive Industry Federation (AIVAM). (2023). Morocco Automotive Sector Report 2023. Casablanca.

[2] IATF 16949:2016. Quality Management System Requirements for Automotive Production. International Automotive Task Force.

[3] IEA. (2024). Global EV Outlook 2024. Paris: International Energy Agency.

[4] CAPMAS. (2024). Egyptian Foreign Trade Statistics — Automotive Sector. Cairo: Central Agency for Public Mobilization and Statistics.

[5] McKinsey & Company. (2023). The Future of Mobility: EV Supply Chain Opportunities for Emerging Markets. McKinsey Center for Future Mobility.

Creative gold for your inbox

Get the latest articles and news delivered straight to your inbox. Subscribe now to stay informed.